Master Compliance in Finance Industry | UK Strategies

Why Compliance Actually Matters Beyond The Rulebook

Imagine compliance not as a rigid set of rules, but as the essential scaffolding that supports the entire financial system. It's the quiet guardian that protects consumers, secures investments, and underpins market integrity. Let’s move beyond the textbook definitions and explore the real-world impact of compliance.

Through conversations with compliance officers at leading UK firms, we’ve discovered how they’ve transformed regulatory obligations into strategic advantages. Instead of seeing compliance as a burden, they view it as a catalyst for innovation and sustainable growth.

This screenshot of the Financial Conduct Authority (FCA) website emphasizes their consumer-focused mission. The prominent placement of information for individuals highlights the FCA’s commitment to protecting consumers and maintaining market stability.

Building Trust, Not Just Following Rules

The most effective compliance teams don't just enforce regulations; they actively cultivate trust. They function as internal partners, collaborating with colleagues to understand business objectives and develop solutions that satisfy both regulatory requirements and operational needs. This collaborative method ensures compliance is woven into the fabric of the organization, not treated as a separate, bolt-on function.

For instance, one UK bank saw a significant improvement in customer satisfaction after implementing a comprehensive compliance program. By streamlining processes and increasing transparency, they strengthened customer relationships and gained a competitive advantage. This illustrates how a robust compliance framework can build customer loyalty and bolster a company's reputation.

Preventing Disasters and Saving Millions

Forward-thinking compliance strategies are more than just avoiding penalties; they are about preventing catastrophic events. By proactively identifying and mitigating risks, UK firms can avoid costly legal disputes, safeguard their reputations, and retain valuable customer trust. Real-world examples demonstrate the substantial financial benefits of effective compliance.

One UK investment firm, for example, averted millions in potential fines by implementing a robust anti-money laundering (AML) program. By identifying suspicious transactions early, the firm prevented illicit activities and avoided regulatory scrutiny. This proactive approach showcases how compliance can act as a powerful shield against financial crime and protect a company's bottom line.

Compliance as a Strategic Differentiator

Leading UK financial institutions recognize that compliance is a key differentiator in the market. In an environment where trust is paramount, a demonstrable commitment to ethical conduct and strong risk management attracts customers and investors seeking stability and reliability. This dedication to compliance builds confidence and fosters long-term relationships. It signifies a firm's commitment not only to profits but also to conducting business with integrity. This approach strengthens the entire financial ecosystem, making it more resilient and trustworthy.

Navigating The UK's Regulatory Ecosystem Like A Pro

This screenshot from the Bank of England website highlights its role in maintaining financial stability. Notice the focus on current economic data and policy updates. This shows how actively the Bank works to shape the financial environment – a core aspect of the broader regulatory landscape.

This illustrates how intertwined financial stability and effective compliance are. For any firm operating in the UK, understanding this is essential.

Understanding the Key Players: FCA, PRA, and OTSI

The UK's financial regulatory structure can appear complicated, but it boils down to a few key bodies. The Financial Conduct Authority (FCA) is like a watchdog, protecting consumers and ensuring market integrity. They're there to make sure financial products and services are fair, transparent, and meet rigorous standards. Imagine them as the customer's champion, constantly on the lookout for bad practices.

Then there’s the Prudential Regulation Authority (PRA). They focus on the financial health of banks, building societies, credit unions, insurers, and major investment firms. Think of them as guardians of financial stability, ensuring these institutions have enough capital and manage their risks well. This protection prevents the entire system from collapsing.

Emerging Regulations and Trends

Financial regulations are always changing to keep pace with the world. A critical area is anti-money laundering (AML) and sanctions enforcement. For example, in 2025, the FCA is significantly investing in financial crime intelligence and data, with a focus on improving firms’ AML and sanctions systems.

The Office of Trade Sanctions Implementation (OTSI), launched in October 2024, plays a vital role in managing sanctions, an area that’s expected to remain a high priority. Want to learn more? Check out these regulatory developments: Insights on UK Financial Services Regulation in 2025

This means keeping up with these changes is crucial for staying compliant. It's not just about knowing the current rules, but also anticipating future ones. This proactive approach is key to thriving in such a dynamic environment.

Staying Ahead of the Curve

Successfully navigating UK financial regulations requires a proactive approach. By understanding what each regulator prioritizes, you can anticipate changes and adapt your strategies. This not only minimizes risk, but can also unlock opportunities for growth and innovation.

Understanding the “why” behind regulations is just as important as the “what.” Grasping the motivations driving regulatory change helps you position your organization for long-term success. This forward-thinking approach allows firms to anticipate and prepare, transforming potential hurdles into strategic advantages.

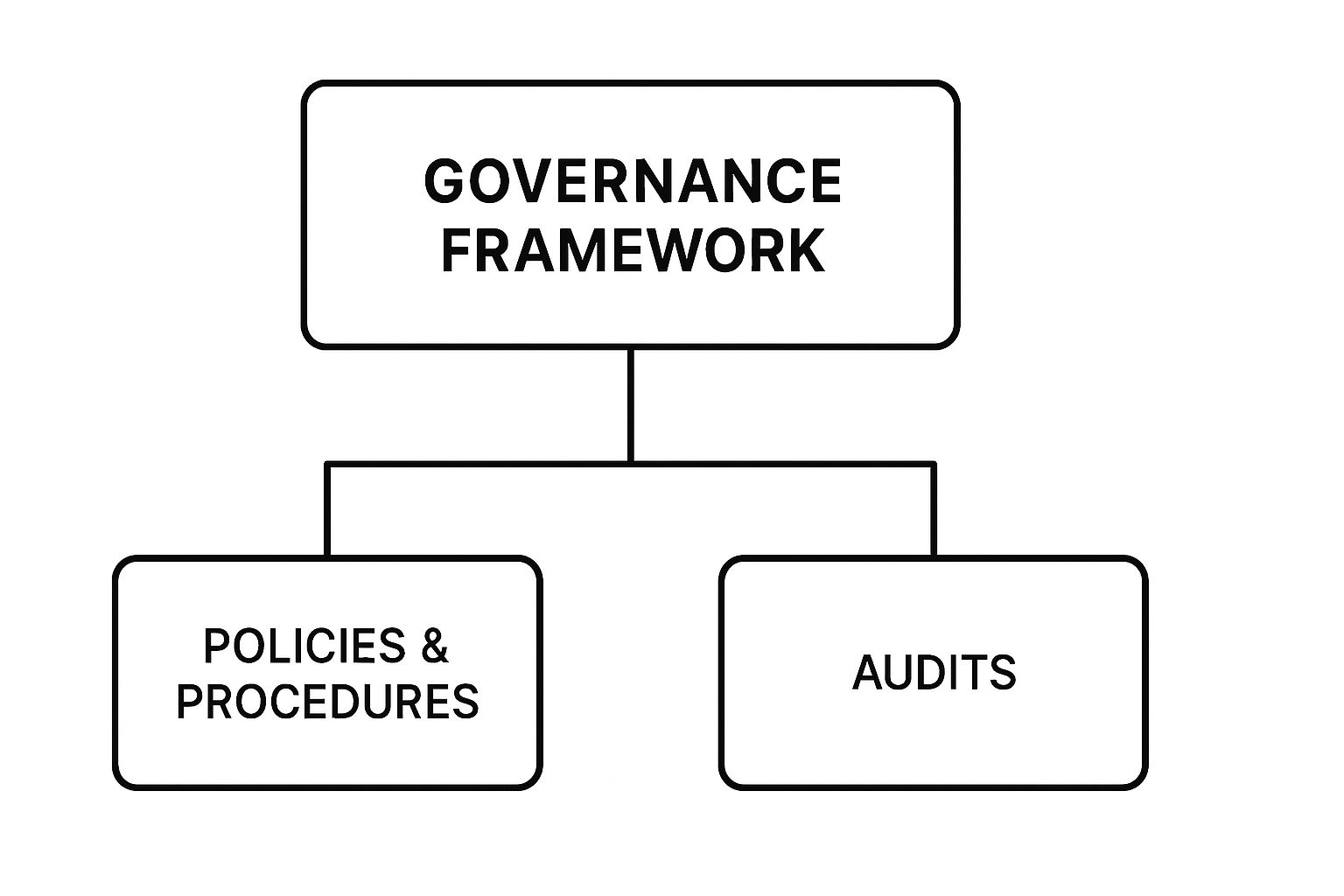

Building Frameworks That Work In The Real World

The infographic above neatly visualizes how a firm's overall Governance Framework, its specific Policies & Procedures, and regular Audits all work together. Think of it as a layered cake: the framework is the base, the policies and procedures are the filling, and the audits are the icing on top. This tiered approach ensures compliance in the finance industry starts with solid foundations and is continually checked for effectiveness.

A robust governance framework provides the guiding principles—the “why” behind everything. Detailed policies and procedures translate those principles into actionable steps—the “how.” Regular audits then confirm that these steps are being followed correctly. This creates a continuous cycle of improvement, ensuring your compliance program is always getting better. But simply having a framework on paper isn't enough. It needs to actually work in practice.

Adapting the Three Lines of Defence

Many UK financial firms use the Three Lines of Defence model. Imagine it like a castle with three walls protecting it. The first line, operational management, is the outer wall, managing risk every day. The second line, risk and compliance functions, is the middle wall, overseeing and challenging the first line’s work. Finally, the third line, internal audit, is the inner keep, providing independent assurance.

Let's bring this to life with an example. Imagine a bank's loan approval process. The loan officer (first line) assesses if the applicant can repay the loan. A compliance officer (second line) checks if the loan officer followed all the rules. Internal audit (third line) then steps back and reviews a sample of loans to verify the whole system is working as intended. This multi-layered approach provides a comprehensive safety net for managing risk.

Integrating Risk and Compliance

Traditionally, risk and compliance functions were like separate departments in a hospital, each focused on their own specialty. Now, smart UK firms are integrating these functions, recognizing the benefits of a more joined-up approach. This integrated view streamlines processes, avoids duplicated effort, and fosters better communication and collaboration.

Think of two doctors, one specializing in cardiology and the other in pulmonology, working together to treat a patient with a complex condition. By sharing their expertise, they provide better overall care. Similarly, integrated risk and compliance teams can better protect the firm from all angles.

Building Practical Processes

Compliance frameworks must be practical and easy to use. Overly complex processes can lead to employees finding shortcuts, which actually increases the risk of non-compliance. Processes should be clear, concise, and simple to follow.

Visualize a fire escape route. It needs to be obvious and easy to access, not hidden away or requiring a complex set of instructions. Compliance processes should be just as straightforward. This ensures compliance is embedded in everyday operations, not something people try to avoid.

To help you choose the best framework for your firm, we've put together a handy comparison table.

Let’s take a look at some popular frameworks and how they stack up against each other:

Compliance Framework Comparison for UK Financial Firms

Comparison of popular compliance frameworks showing implementation complexity, regulatory alignment, and effectiveness for different firm sizes

| Framework | Implementation Time | Regulatory Alignment | Best For | Key Benefits |

|---|---|---|---|---|

| COSO | 6-12 months | Strong | Large firms | Comprehensive risk management |

| COBIT | 3-6 months | Moderate | Medium-sized firms | IT governance and control |

| NIST Cybersecurity Framework | 12-18 months | Strong | Firms with high cybersecurity risk | Robust cybersecurity posture |

| ISO 27001 | 9-12 months | Strong | Firms handling sensitive data | Data security and privacy |

As you can see, each framework has its own strengths and weaknesses. Choosing the right one depends on factors like your firm’s size, industry, and specific risk profile.

By making compliance a natural part of the workflow, firms can strengthen their overall compliance posture and foster a culture of responsibility. This proactive approach helps to prevent problems before they arise, protecting both the firm and its customers.

When Fraud, Credit, and Compliance Stop Fighting Each Other

Traditionally, fraud, credit, and compliance teams within financial institutions have functioned much like isolated islands. Picture three expert mechanics, each assigned to the same car, yet stubbornly refusing to share tools or even talk to each other. One is engrossed in the engine (fraud), the next preoccupied with the brakes (credit), while the third focuses solely on ensuring the vehicle adheres to road safety regulations (compliance). This disjointed approach often leads to wasted effort, overlooked insights, and heightened vulnerabilities.

However, a noticeable shift is occurring within the UK financial services sector. Progressive institutions are beginning to grasp the substantial benefits of integrating these crucial functions. This movement is propelled by the escalating complexity of financial crime, coupled with the ever-increasing burden of regulatory requirements.

In recent years, a significant trend toward converging fraud, credit, and compliance has emerged. This integration is largely driven by the growing intricacies of financial crime and the mounting pressure of regulations. For example, by 2025, UK financial services are projected to grapple with significant challenges in minimizing operating expenses related to risk and compliance, all while navigating stringent regulatory demands. Want to delve deeper into this developing trend? Explore further here: Convergence of Fraud, Credit, and Compliance

This convergence isn't simply a passing fad; it signifies a fundamental transformation in how firms manage risk and maintain compliance within the financial industry.

Breaking Down Silos: A Unified Approach

Integrating these teams offers a more comprehensive perspective on risk. Imagine those mechanics finally deciding to pool their knowledge. They share their individual expertise, enabling them to detect potential issues earlier and devise more effective solutions. This unified approach not only cuts costs but also boosts overall performance. By openly communicating and working in unison, they ensure the entire vehicle operates smoothly and safely.

This collaborative strategy empowers organizations to identify risks sooner, react more swiftly to emerging threats, and enhance operational efficiency. For instance, a centralized database of suspicious activity could equip both fraud and credit teams to pinpoint potential problems more rapidly, preventing financial losses and safeguarding customers.

Real-World Implementation: Lessons Learned

The path toward integration isn't without its hurdles. Unifying teams with distinct cultures, priorities, and performance indicators can be a complex endeavor. It's akin to merging three separate companies, each with its own established practices. However, the potential rewards significantly outweigh the challenges.

Through in-depth case studies, we'll examine how UK firms are successfully navigating this transition. Learn from real-world implementation experiences – both the successes and the hard-learned lessons. We'll explore the human element, technological considerations, and regulatory ramifications of this convergence. This might pique your interest: Financial Services Public Relations

These practical examples offer invaluable insights for organizations considering or currently undertaking this crucial integration. They provide a practical guide to addressing common obstacles and achieving positive outcomes.

Building a Stronger Future: Attracting Top Talent

Integrated strategies for fraud, credit, and compliance also foster compelling new career development prospects. This can be instrumental in attracting and retaining top-tier professionals in a competitive job market. By providing cross-functional training and exposure to diverse areas of expertise, firms can cultivate a more dynamic and engaging work environment. This benefits both the individual employees and the organization as a whole.

This fosters a beneficial cycle. A more collaborative and effective risk management function bolsters the firm's reputation and attracts talented individuals, further strengthening its capacity to manage risk and prosper in a demanding regulatory landscape.

Protecting Vulnerable Customers While Building Better Business

The image above shows a customer talking with a financial advisor. This interaction gets to the heart of the Consumer Duty: earning trust and ensuring good outcomes for customers, especially those facing difficult situations. It means moving beyond simply selling and truly understanding individual needs. This focus on customer well-being is changing how the UK financial industry operates.

The Consumer Duty isn't just another regulation to check off a list; it’s a complete change in how UK financial firms work with their customers. Think of it as shifting from a one-time transaction to building an ongoing relationship. This requires firms to understand the real-life impact of their products and services, especially on those who might be more vulnerable.

Imagine a customer grieving a recent loss. A firm following the Consumer Duty would offer personalized support and understanding, not just follow a standard script.

Financial services regulation in the UK is constantly changing, with a growing emphasis on protecting customers, especially those in vulnerable situations. In 2025, the FCA plans to review how firms treat vulnerable customers, making sure it aligns with the Consumer Duty. This initiative is all about ensuring firms offer proper support and protection, reinforcing the importance of compliance in maintaining customer trust. Learn more about UK Financial Services Regulation in 2025. This highlights how crucial it is for firms to prioritize customer well-being and develop robust systems for identifying and supporting these customers.

Identifying and Supporting Vulnerable Customers

Leading UK firms are developing ways to identify vulnerable customers without making them feel singled out. This involves thoughtful language, processes, and staff training. It's about creating an environment where customers feel safe sharing their situation.

Some firms use data analysis to find potential signs of vulnerability, such as a sudden change in spending. This information then alerts trained staff to reach out and offer the right kind of support.

But identifying vulnerable customers is just the beginning. Firms also need to design support systems that people will actually use. This could mean offering flexible payment plans, making complicated processes simpler, or giving access to expert advisors.

It's about removing barriers and making it as easy as possible for vulnerable customers to get the help they need. This could be as simple as using larger font sizes on documents or offering appointments outside of normal business hours. Explore more on Digital Marketing for Financial Services.

Measuring Success Beyond Compliance

Measuring how well vulnerability frameworks work is essential. Successful firms track metrics that not only satisfy regulators but also show improvements in their business. These metrics might include customer satisfaction scores, how quickly complaints are resolved, and how many people use support services.

By showing a clear connection between customer well-being and business success, firms can demonstrate the value of investing in these initiatives.

This approach helps align regulatory requirements with business goals. For example, if a firm reduces customer churn by providing good vulnerability support, it shows both compliance with the Consumer Duty and improved financial performance. This creates a win-win and strengthens the argument for continued investment in customer-focused programs.

Overcoming Implementation Challenges

Putting vulnerability frameworks in place comes with its own set of difficulties. Sales teams might resist shifting their focus from sales targets, it can be hard to measure results, and it’s inherently complex to balance individual needs with efficiency.

Openly discussing these challenges is vital. It's about acknowledging the difficulties and working together to find solutions.

Some firms have succeeded by rewarding sales teams based on customer satisfaction, not just sales numbers. This change encourages a more customer-centered approach. This kind of creative thinking ensures the whole organization is working toward the same goal: providing excellent service to all customers, especially those in vulnerable circumstances.

To help you measure the effectiveness of your Consumer Duty compliance, let's look at some key areas to track:

The following table provides a framework for monitoring compliance effectiveness:

Consumer Duty Compliance Outcomes Tracking

Key metrics and indicators for measuring Consumer Duty compliance effectiveness across different customer segments

| Outcome Area | Key Metrics | Measurement Frequency | Regulatory Expectations | Success Indicators |

|---|---|---|---|---|

| Products & Services | Customer complaints, Product returns | Monthly | Clear, fair, and not misleading | Low complaint rates, Positive customer feedback |

| Price & Value | Customer churn rate, Price comparison data | Quarterly | Fair value for customers | Competitive pricing, High customer retention |

| Customer Support | Resolution time, Customer satisfaction scores | Monthly | Accessible and effective support | Prompt resolution, High satisfaction scores |

| Consumer Understanding | Customer feedback surveys, Market research data | Annually | Understanding customer needs | Actionable insights, Improved product design |

Tracking these metrics allows firms to demonstrate real progress in meeting the Consumer Duty requirements and build a strong case for their compliance efforts. This careful approach ensures vulnerability support is not just an idea but a practical reality for all customers.

Technology That Actually Makes Compliance Easier

Imagine trying to manage financial compliance manually. Spreadsheets overflowing, regulations changing constantly – a real headache, right? Now picture this: a system humming along in the background, catching potential issues before they become problems, handling the tedious tasks, and letting your team focus on the big picture. That's the power of RegTech, and it's reshaping how UK firms handle compliance.

This Wikipedia screenshot gives a helpful snapshot of what Regulatory Technology (RegTech) is all about – using technology to tackle regulatory hurdles. It really highlights how essential technology has become in navigating today's complex regulatory environment. This blend of tech and regulation is the key to making compliance both efficient and effective.

From Demo to Value: Real-World RegTech

Lots of RegTech solutions have dazzling demos, but the real test is whether they deliver on the front lines of your daily operations. Let's look at some real-world examples of AI-powered monitoring, automated reporting, and integrated risk platforms – exploring what worked, what fell short, and the reasons why.

Think about this: a UK bank implemented an AI system to analyze transactions for anything suspicious. Not only did it flag potential fraud, but it also learned and adapted to changing criminal tactics. This meant fewer false alarms and more time for human analysts to investigate complex cases. This shows how AI can really boost the effectiveness of compliance efforts.

Choosing the Right Tools: Evaluating Vendors

Picking the right RegTech vendor takes a practical approach. Don't get distracted by shiny bells and whistles; focus on solutions that solve your specific problems. Ask the hard questions about implementation, integration, and ongoing support.

For instance, think about how the new tech will work with your current systems. What kind of training and support will you get? These practical considerations are vital.

You also need to consider the future. Will these new systems grow with your firm and adapt to changing rules? Make sure they're scalable and flexible. This long-term view protects your investment and ensures your compliance tech stays relevant. You might also find this interesting: SEO for Financial Services.

Human Oversight in an Automated World

Automation is great, but human oversight is still essential. Technology should empower people, not replace them. Think of it like a self-driving car – it handles the routine stuff, but the driver stays alert and ready to take over if needed.

This means compliance professionals need new skills. Instead of manual tasks, they'll need to be experts in data analysis, understanding AI-generated insights, and making smart decisions based on that information. This keeps technology a powerful tool under human control.

Building the Business Case and Managing Change

New tech needs buy-in from everyone involved. This means building a solid business case. Show how automation will cut costs, boost efficiency, and lower risk. Be prepared to talk about job changes and how to manage the transition.

Open communication is crucial. Involve your teams from the start to address their concerns and make the shift smoother. This builds support and minimizes resistance to the new tech.

By focusing on practical uses and a people-first approach, firms can use technology not just to tick compliance boxes, but to make operations smoother and improve overall risk management. This forward-thinking approach sets up UK financial institutions for success in a constantly changing regulatory landscape.

Creating a Compliance Culture That Survives Bad Days

Building a genuine compliance culture isn’t like flipping a switch. It's more like nurturing a delicate plant. It requires dedicated care, consistent attention, and the right environment to flourish. Think of your compliance policies as seeds planted in the fertile ground of a supportive company structure. Regular training and communication are the water and sunlight needed for strong roots – deeply embedded compliance practices – to take hold.

This section explores how top UK financial institutions are cultivating robust compliance cultures that withstand even the toughest storms. This involves creating an environment where compliance isn't just a checkbox, but a fundamental value woven into every decision.

Fostering Open Communication and Difficult Conversations

Successful firms encourage open discussions about compliance, even when the topics are uncomfortable. They understand that mistakes happen. Think of it as a regular check-up for your compliance program. It's not about pointing fingers, but about identifying weak spots and making sure everyone's on the same page.

These conversations are vital for building a culture of learning and improvement. One UK firm, for instance, runs regular “compliance clinics” where employees can ask questions and voice concerns without fear of judgment. This proactive approach nips potential issues in the bud.

Maintaining Momentum During Stressful Periods

When deadlines loom and the pressure mounts, compliance can sometimes slip down the priority list. However, strong compliance cultures resist this urge. They know that upholding compliance, especially during stressful periods, is like having a robust immune system – it shields the organization from potentially harmful consequences.

Successful firms weave compliance into their daily routines. They integrate compliance processes into existing systems, making it easy for staff to follow them even when things get hectic. This way, compliance becomes second nature, not an added burden.

Adapting Strategies for Different Business Areas

A one-size-fits-all approach to compliance rarely hits the mark. Different areas within a financial institution encounter unique obstacles and risks. It's like designing a fitness plan – what works for a marathon runner won't necessarily work for a weightlifter.

Leading firms customize their compliance strategies to suit specific business functions. For example, the compliance demands of a trading desk are different from those of a customer service team. This tailored approach ensures compliance efforts are both relevant and effective.

Measuring Cultural Health and Identifying Warning Signs

Regularly checking the health of your compliance culture is crucial. It's like glancing at your car’s dashboard – it tells you if things are running smoothly or if there’s trouble brewing. This means gathering data and looking out for early red flags that could signal potential problems.

Some firms use regular surveys to get a feel for staff attitudes towards compliance. Others track key metrics like the number of near misses or compliance breaches reported. These data points offer valuable insights into the effectiveness of the existing compliance program.

Course Correction: Fixing Compliance Culture Drift

Even with the best of intentions, compliance cultures can stray off course over time. This can happen due to things like employee turnover, regulatory changes, or simply complacency. It's like a ship slowly drifting off course – small corrections are needed to stay on track.

Top UK institutions have systems in place to detect and rectify these deviations. They conduct regular compliance audits, review their policies and procedures, and provide refresher training to keep everyone up to speed. This constant vigilance keeps compliance front and center.

Adapting to Remote and Hybrid Working

Remote and hybrid work models present fresh challenges for compliance. Maintaining a strong compliance mindset when employees are scattered requires creative thinking. It's like conducting an orchestra remotely – you need new strategies to ensure everyone plays in harmony.

Some firms have launched virtual compliance training programs and online communication channels to stay connected with remote staff. Others have adopted tech solutions that provide secure access to compliance information from anywhere. These adjustments help maintain a shared sense of responsibility for compliance, even in a virtual world.

Creating a robust compliance culture is a continuous process that demands effort and adaptation. But the payoff – a stronger, more resilient organization – makes it a worthwhile investment. By adopting these practices, UK financial institutions can ensure their compliance not only weathers the storms but thrives in the face of any challenge.

Looking to raise your brand's profile and manage the intricate world of financial compliance? Blackbird Digital, a leading UK marketing agency specializing in digital PR and SEO, can help. We build engaging stories and secure features in top publications to boost your brand’s visibility and credibility. Learn more about how Blackbird Digital can support your compliance and marketing efforts.